If I Work ON My Business What Should I Be Doing?

Ever wondered what it actually means to work ‘on’ your business as well as working ‘in’ your business? You’re not the only one, so let’s break it down.

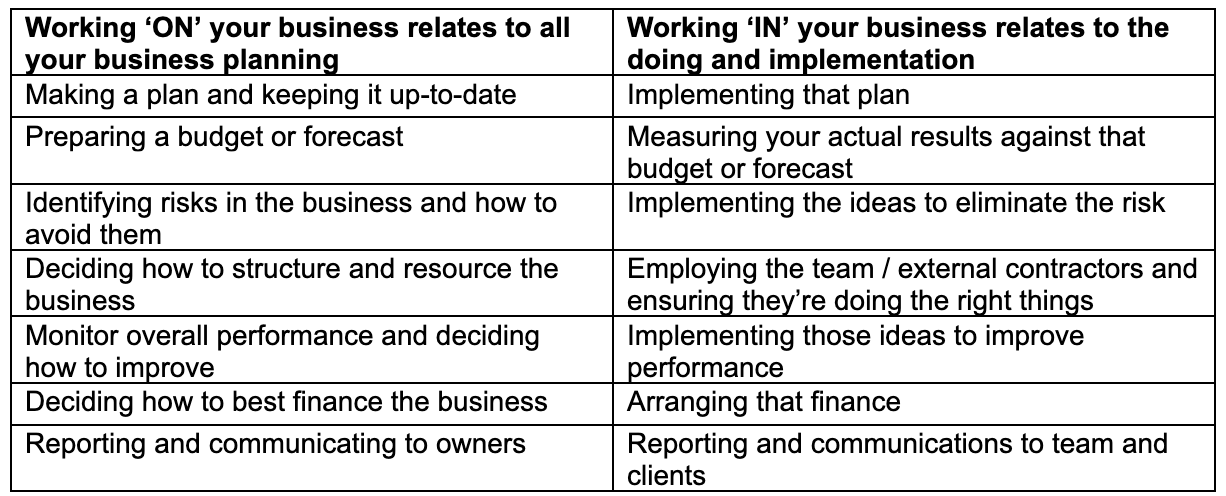

First, here are some practical distinctions to compare working ‘on’ and working ‘in’.

Now that the key differences have been explained, here are the five most important activities you should be doing with your business to drive success:

-

- Prepare a business plan and update it annually. Tip : Do this in the last month of your financial year or the first month of the new financial year

- Prepare a budget and forecast for the upcoming 12 months. Tip : Do this at the same time as you prepare your plan (and of course, review this annually too)

- Report against that plan and budget monthly

- Communicate the plan and the results to the owners and your team

- Meet monthly for 1 to 2 hours to review your progress, your numbers, your business structure and any risks and opportunities that exist to improve the business

How much time should you set aside to work on your business?

Working on the business doesn’t need to be a full-time role, but you should make sure you’re allocating sufficient time each week to focus on it.

A good guideline is to be working on your business 1 to 2 hours each week, while allowing for a half-day progress check in each month to make sure you’re on track.

Also, set aside 1 to 2 days each year to go off-site and update your business plan and structure. Best practice is to get someone independent of your business to help you establish and maintain these regular disciplines and hold you to account to really improve your business.

What do you need to change to work more effectively ‘on’ your business?

If you need our help, get in touch.

“The business is there to serve you, not the other way round. You should not be a slave to your business” – Anon

The following content was originally published by BOMA. We have updated some of this article for our readers.